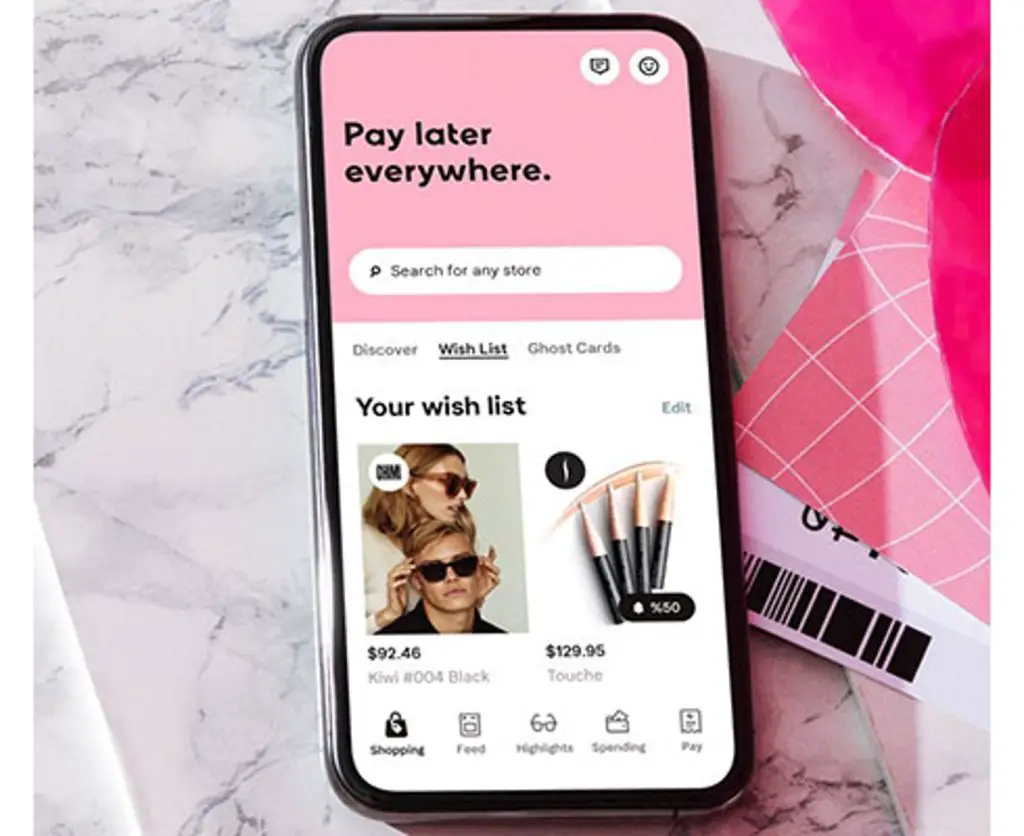

Buy now pay later applications are increasingly favored for financing purchases. Enterprises such as Affirm, AfterPay, and Klarna enable you to divide the expense of everyday items – from sneakers to groceries – into multiple installments.

The pay-in-four loan structure is prevalent. Initially, you’re obliged to make a modest down payment, typically around 25%, then commit to automatic payments via a credit or debit card for the subsequent three installments, often spaced two weeks apart.

Recently, the option to buy now, pay later has become more accessible at a renowned grocery and retail chain.

This might appear appealing compared to credit cards, as pay-in-four schemes typically don’t levy interest charges.

5 Dangers of Buy Now Pay Later

Delaying upfront payment for a purchase might seem convenient, but it’s important to be cautious of the risks associated with utilizing BNPL services.

1. Buy Now, Pay Later Could Hurt Your Credit

Merely applying for a buy now, pay later service doesn’t have a negative impact on your credit score because these companies typically do not conduct a hard credit check on your credit history.

However, BNPL loans affect your credit profile in alternative ways.

Unlike credit card providers, most BNPL companies do not share all of their transaction data with the three major credit reporting agencies – TransUnion, Equifax, and Experian.

Consequently, making on-time payments on BNPL loans does not contribute to the enhancement or establishment of your credit score.

The current framework for credit reporting isn’t optimized for short-term revolving lines of credit, such as buy now, pay later loans. Credit reporting agencies are endeavoring to address this issue with BNPL companies, but progress is ongoing.

If BNPL companies were to report all of their data to credit bureaus within the existing system, it could potentially have adverse effects on consumers’ credit scores, even if payments were made punctually.

Conversely, failing to make a payment on a BNPL plan can negatively impact your credit score.

If you consistently miss payments, your debt may be transferred to a debt collection agency and subsequently reported to a credit bureau, potentially leading to a decrease in your credit scores.

2. Buy Now Pay Later Encourages You to Overspend

By its very design, BNPL services entice consumers to increase their spending and borrowing, creating a potentially risky pattern of overspending.

Acknowledging the ease with which individuals can fall into this pattern, financial experts emphasize the deceptive nature of these seemingly small payments. Despite their appearance, these payments can quickly accumulate into significant expenses.

According to a March 2022 report by the Financial Health Network, approximately 30% of surveyed BNPL users admitted to spending more than they typically would have without access to BNPL services

*Check out our 8 Ways To Pay Off Your Debt article.*

Similarly, data from a Consumer Reports survey indicated that 45% of BNPL users acknowledged that they would not have been able to afford their purchases without the option to buy now and pay later.

3. You Could Face Late Fees

Each buy now, pay later company implements distinct terms and conditions regarding the consequences of falling behind on payments.

While some companies, such as Affirm and PayPal’s Pay in 4, may not impose any late fees at all, others like Afterpay and Zip do charge late fees, ranging up to $8 and $10 respectively.

Late fees associated with buy now, pay later applications are increasingly prevalent, as indicated by a September 2022 report from the Consumer Financial Protection Bureau. The report found that 10.5% of unique users incurred at least one late fee in 2021, up from 7.8% in 2020.

*To avoid falling behind on payments, learn more about managing debt with our How to Use the Debt Snowflake Method *

4. You’re More Likely to Overdraft

In 2021, nearly 90% of buy now, pay later users opted to link a debit card for automatic loan payments, as reported by the CFPB. Recent academic studies indicate that BNPL users are more prone to incurring overdraft fees from their bank compared to non-users.

The average overdraft fee amounts to approximately $30.

All five major BNPL companies make multiple attempts to reauthorize failed payments, sometimes up to eight times for a single installment, according to the CFPB.

This means that if a BNPL company continues to try to process a payment with insufficient funds, you could potentially face multiple overdraft fees from your bank in a short period.

5. BNPL Companies Push Products Directly to Consumers

For years, buy now, pay later companies have enticed shoppers to split their purchases at online checkout. However, their strategies have evolved, with a focus on engaging consumers through app-driven models.

According to a September 2022 report by the CFPB, in the app-driven model, BNPL lenders primarily serve as marketing platforms, directing customers to retailers through referral clicks.

Furthermore, BNPL lenders often gather user data to tailor product features and marketing campaigns based on individual buying preferences.

As a result, even when consumers aim to save money and adhere to their budgets, these companies introduce additional challenges.

Conclusion

The rise of buy now, pay later (BNPL) services presents both opportunities and challenges for consumers. While BNPL offers convenience and flexibility, allowing shoppers to spread out payments over time, it also comes with risks such as overspending, late fees, and potential impacts on credit scores.

Recent trends indicate that BNPL companies are evolving their strategies, moving beyond simply facilitating payments at checkout to actively engaging consumers through app-driven models. This shift not only serves as a marketing platform for retailers but also enables BNPL lenders to collect user data to tailor marketing campaigns and product features.

As consumers navigate the landscape of BNPL services, it’s crucial to exercise caution and make informed decisions. Understanding the terms and conditions of BNPL agreements, monitoring spending habits, and staying vigilant about potential fees and impacts on credit are essential steps in managing the use of these services responsibly.