Navigating the world of personal finance can be daunting. With countless strategies and methods available, finding a simple and effective approach to budgeting can be a challenge. Enter the 50/30/20 rule.

This budgeting method, popularized by U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi, offers a straightforward way to manage your income. It divides your after-tax earnings into three categories: needs, wants, and savings or debt repayment.

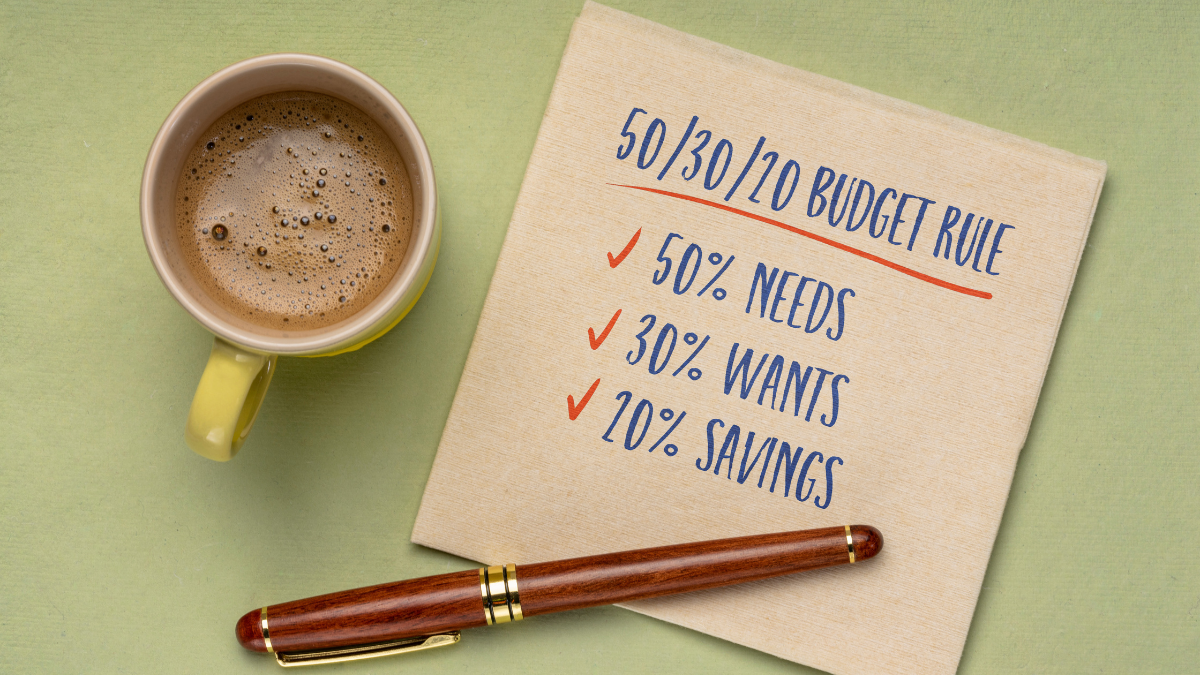

The rule suggests that 50% of your income should go towards needs, such as housing and groceries. Another 30% is allocated for wants, like dining out or entertainment. The remaining 20% is directed towards savings or paying off debt.

But how can you implement this rule effectively? And how can it help you achieve your financial goals?

- What is the 50/30/20 Rule?

- The Origins of the 50/30/20 Rule

- How the 50/30/20 Rule Works

- Tools to Help Implement the 50/30/20 Rule

- Adapting the 50/30/20 Rule to Your Financial Situation

- The Benefits of the 50/30/20 Rule for Money Management

- Common Questions and Misconceptions About the 50/30/20 Rule

- Tips for Success with the 50/30/20 Rule

- Conclusion: Taking Control of Your Financial Future

What is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting framework designed to simplify personal finance. By dividing income into three distinct categories, it offers clarity and structure to financial management.

What are the Three Categories?

The rule categorizes expenses into needs, wants, and savings or debt payments. Each category is assigned a percentage of your after-tax income, promoting intentional financial allocation.

- Needs (50%): Essential expenses like rent, groceries, utilities, and insurance.

- Wants (30%): Non-essential spending like dining out, hobbies, and entertainment.

- Savings and Debt Repayment (20%): Funds directed towards savings accounts, investments, or paying off debts.

The beauty of the 50/30/20 rule lies in its simplicity. It helps demystify budgeting by breaking it into easy-to-manage parts. Each category has its purpose, making it easier to prioritize financial decisions.

Why is it Effective?

This method promotes a balanced approach to money management. By encouraging you to fulfill essential needs while allowing for enjoyment, the rule stresses the importance of saving and reducing debt.

Who Can Benefit from This Rule?

The 50/30/20 rule is versatile and suitable for various income levels. Whether you’re a student, a young professional, or planning for retirement, this method can assist in achieving financial goals.

The rule is also flexible. Adjustments can be made based on individual circumstances, making it an adaptable tool in personal finance. It supports both beginners and seasoned budgeters seeking to refine their spending habits.

The Origins of the 50/30/20 Rule

The 50/30/20 rule was popularized by U.S. Senator Elizabeth Warren. She, along with her daughter Amelia Warren Tyagi, introduced this simple budgeting technique in their book “All Your Worth: The Ultimate Lifetime Money Plan.” Their work aimed to make money management accessible to everyone.

Originating in the early 2000s, the rule emerged as a response to complex financial strategies. Warren and Tyagi wanted a straightforward method that ordinary people could follow without needing advanced financial knowledge. They believed that clear financial guidelines could help individuals achieve stability and control over their finances.

By breaking income into three primary categories, their rule offered a new perspective on income distribution. It was designed to promote both financial health and well-being, encouraging a balance between necessary expenses, leisure, and future savings. Their approach continues to resonate, offering relevance in today’s economic landscape.

How the 50/30/20 Rule Works

The 50/30/20 rule simplifies budgeting by dividing after-tax income into three main categories. This method emphasizes practicality and structure, making it accessible and easy to implement. The clear breakdown helps individuals focus on what truly matters in their financial lives.

First, 50% of income is allocated for essential needs. These are unavoidable expenses, such as housing, food, and utilities. Prioritizing needs ensures that these fundamental expenses are covered, reducing stress and uncertainty.

Next, 30% is dedicated to wants. Wants represent discretionary spending on things that enhance lifestyle, like dining out and hobbies. While these expenses are not essential for survival, they contribute to happiness and quality of life.

Finally, the remaining 20% is earmarked for savings and debt repayment. This allocation encourages building an emergency fund and paying off existing debts. Saving and investing early can lead to long-term wealth building and financial security.

Key elements of the 50/30/20 rule:

- 50% for essential needs

- 30% for discretionary wants

- 20% for savings and debt repayment

Allocating for Needs: The 50%

Understanding your financial needs is vital for successful budgeting. Needs encompass essential expenses required for daily living. These are non-negotiable and must be prioritized to maintain stability and well-being.

Housing typically consumes a significant portion of the 50%. This includes rent or mortgage payments, along with utilities. Ensuring your living space is covered provides a solid foundation for all other financial decisions.

Transportation and healthcare also fall under this category. Consider public transit, car expenses, and health insurance premiums. These costs can fluctuate, so it’s vital to monitor them closely.

Groceries and other household essentials complete this list. Striking a balance between affordability and quality is essential here. By accurately tracking these expenses, you can ensure this 50% allocation effectively serves your needs.

Common needs include:

- Rent or mortgage

- Utilities and transportation

- Healthcare and groceries

Budgeting for Wants: The 30%

Wants refer to non-essential items that bring joy and enhance lifestyle. This 30% allocation allows for personal indulgences without jeopardizing financial health. Managing wants effectively can help prevent overspending and maintain balance.

Dining out, entertainment, and travel fall under this category. These activities are often viewed as rewards after fulfilling essential responsibilities. Deciding how much to spend on these can vary based on personal preferences and values.

This category also covers leisure activities, such as hobbies and gym memberships. Identifying which indulgences are most fulfilling can help allocate funds wisely. It’s important to ensure that spending on wants does not compromise essential needs or savings goals.

While wants offer enjoyment, discipline remains crucial. Regularly reviewing this category can help maintain balance and avoid financial pitfalls. By setting boundaries, you ensure both present enjoyment and future security.

Typical wants include:

- Dining and entertainment

- Leisure activities and hobbies

- Fashion and non-essential tech

Prioritizing Savings and Debt Repayment: The 20%

This final 20% focuses on securing your financial future. It emphasizes building savings and reducing existing debts to achieve financial freedom. Consistency is key to seeing significant progress in this area over time.

Emergency funds are a primary focus of this allocation. They provide a safety net for unforeseen expenses, reducing financial stress in emergencies. Starting with even small, regular contributions can make a big difference.

Debt repayment also plays a crucial role here. Prioritizing high-interest debts first can save money on interest and improve your credit score. Gradually clearing debts allows more funds to be redirected toward savings later.

Investments are a powerful wealth-building tool, best included in this category. Whether through retirement accounts or other investment options, they help grow wealth over time. Consistent contributions can lead to significant long-term gains, even with modest starting amounts.

Savings and debt priorities include:

- Building emergency funds

- Paying down high-interest debts

- Growing investments for wealth building

Tools to Help Implement the 50/30/20 Rule

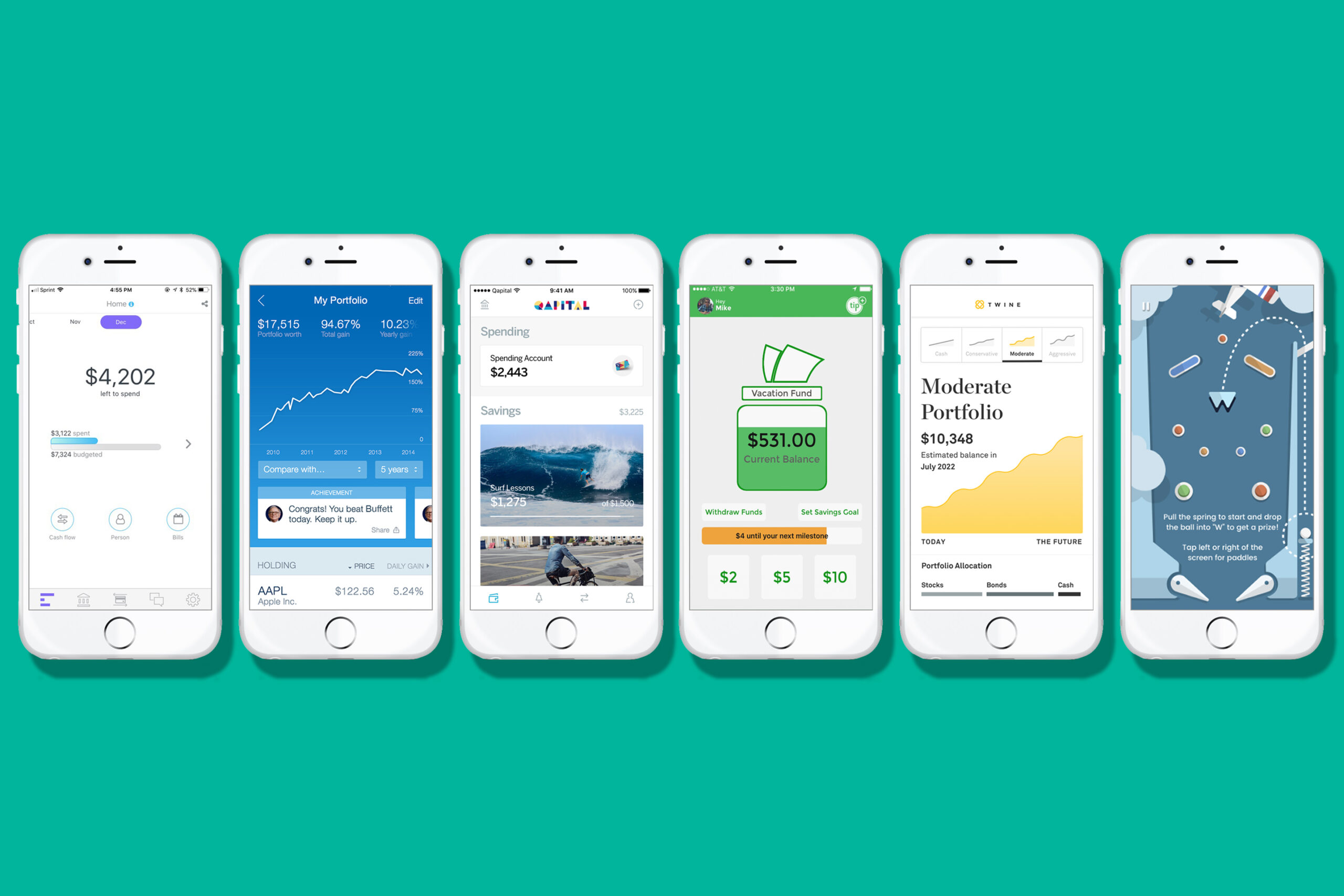

Utilizing the right tools can simplify adherence to the 50/30/20 rule. Many resources are available to help streamline budgeting and financial allocation. Technology plays a crucial role in supporting financial discipline.

Budgeting apps are a popular choice for tracking expenses and income distribution. These apps often offer visual representations, making it easier to comprehend spending patterns. They are designed to keep users engaged and informed about their financial health.

Online banking features also contribute to effective money management. Most banks provide detailed transaction histories and categorization options. This information can assist in aligning spending with the rule’s guidelines, enhancing personal finance management.

Using a 50 30 20 Rule Calculator

A 50/30/20 rule calculator can be a valuable asset in budgeting efforts. It quickly determines appropriate allocation across needs, wants, and savings. Inputting after-tax income offers a clear breakdown for easy planning.

Calculators are designed to provide immediate results. This swift feedback allows users to make quick adjustments if needed. They often include additional features such as debt repayment estimates and savings projections.

This tool reduces the guesswork associated with budgeting. By understanding where money should go, users feel empowered to make informed financial decisions. The clarity this brings can lead to improved financial discipline and goal-setting.

Creating a 50 30 20 Rule Spreadsheet

For more personalized tracking, creating a 50/30/20 rule spreadsheet can be beneficial. Spreadsheets allow users to tailor categories to fit their unique spending habits. This customization helps maintain focus on personal financial goals.

Using a spreadsheet means you can manually input expenses and categorize them. This active involvement increases awareness of spending habits and potential areas for improvement. Regular updates ensure the accuracy of your financial snapshot.

Spreadsheets offer flexibility in how information is displayed and analyzed. From pie charts to detailed lists, they cater to diverse preferences. The insights they offer enable users to make strategic adjustments in line with the 50/30/20 rule.

Adapting the 50/30/20 Rule to Your Financial Situation

The 50/30/20 rule is flexible, allowing adjustments to fit different financial situations. It’s essential to tailor the rule to meet specific needs and goals. Customizing allocations ensures the rule serves your unique circumstances.

Begin by evaluating your current financial landscape. Consider factors such as regular expenses, debt levels, and savings. This assessment will guide necessary modifications to the standard rule percentages. For instance, if debt is high, prioritize reducing it by shifting some “wants” allocation to debt repayment.

For those with irregular income, consider basing budget allocations on average earnings. This approach provides a steady framework during months with fluctuating income. Maintaining stability is key to preventing financial stress when income varies.

A revised allocation might look like the following:

- 60% for needs: When living costs are particularly high.

- 20% for wants: If you are focusing on debt elimination.

- 20% for savings: Ensures ongoing contributions to future financial security.

Remember, the 50/30/20 rule is not rigid. Adjustments that reflect personal priorities and financial realities enhance its effectiveness. Regularly reviewing and updating your budget keeps it aligned with life changes and financial progress. This proactive approach ensures the rule serves as a helpful guide rather than a constraint.

The Benefits of the 50/30/20 Rule for Money Management

The 50/30/20 rule offers numerous benefits that enhance personal finance management. It simplifies budgeting by creating clear categories. This clarity reduces the complexity of tracking various expenses.

One major advantage is its ability to instill discipline in spending habits. By allocating specific percentages, it encourages mindful spending and helps prevent impulse purchases. Financial discipline fosters long-term financial stability.

The rule also facilitates the identification of financial priorities. By focusing on needs, wants, and savings, individuals can quickly distinguish between essential and non-essential expenses. This distinction aids in making informed financial decisions.

Additionally, the 50/30/20 rule supports long-term financial planning. Consistent saving and debt repayment contribute to future financial goals. This approach promotes a balanced financial life that integrates both present enjoyment and future security.

Key Benefits:

- Simplifies budgeting and reduces stress

- Encourages financial discipline and mindful spending

- Prioritizes essential expenses over unnecessary ones

- Supports long-term financial planning and stability

Implementing the 50/30/20 rule equips individuals with a practical framework for effective money management. By fostering financial awareness and conscious decision-making, it paves the way toward financial freedom and well-being.

Common Questions and Misconceptions About the 50/30/20 Rule

The 50/30/20 rule is often praised for its simplicity. However, misconceptions can arise about its universal application. Some believe it suits every financial situation.

A common misconception is that the rule fits everyone perfectly. In reality, it might need adjusting based on personal circumstances and income variability. Flexibility is key to applying this rule effectively.

Others question if focusing on percentages ignores unique financial goals. Yet, these guidelines serve as a starting point. Tailoring them can lead to improved financial awareness and better money management.

Is the 50/30/20 Rule Suitable for Everyone?

While the 50/30/20 rule offers a useful framework, it’s not suitable for everyone. Individuals with high debt or low income may struggle to apply its exact percentages.

In such cases, it’s important to adapt the rule. Adjusting the allocations to prioritize immediate needs or debt repayment can make it more appropriate. Each person should tailor the rule to fit their unique financial landscape.

How to Adjust the Rule for Irregular Income

For freelancers or those with variable income, applying the 50/30/20 rule can seem challenging. It’s crucial to base allocations on average monthly earnings rather than fluctuating income.

Setting aside a buffer for months with lower income is wise. Tracking average income over several months helps stabilize budgeting. Flexibility ensures that the rule remains a useful tool for managing irregular finances.

Can the 50/30/20 Rule Help with Wealth Building?

The 50/30/20 rule can indeed contribute to wealth building over time. Its focus on consistent saving fosters good financial habits that lay the groundwork for future growth.

Allocating 20% toward savings and investments supports long-term financial goals. By emphasizing the importance of saving, this rule can accelerate wealth creation and secure financial stability in the long run.

Tips for Success with the 50/30/20 Rule

Achieving success with the 50/30/20 rule involves more than following percentages. Adjusting the rule to fit your life can lead to better outcomes. Stay flexible and reevaluate your budget as needed.

Tracking your expenses is crucial to truly grasp your financial habits. Regularly reviewing these can help you pinpoint where you might overspend. This awareness is a step towards better financial control.

Communication plays a key role, especially for families. Involving partners or family members in budgeting discussions ensures everyone is aligned with financial goals. An open dialogue can prevent misunderstandings and encourage teamwork in managing money.

Here are some tips for maximizing this budgeting method:

- Start small: Begin with minor adjustments to your current spending.

- Set clear goals: Identify what you want to achieve with your budget.

- Use tech tools: Leverage apps to track and manage expenses.

- Regular check-ins: Review your budget monthly to make sure it aligns with your goals.

- Reward progress: Celebrate milestones to stay motivated on your financial journey.

Staying proactive in these areas can make the 50/30/20 rule an effective tool. Over time, these practices enhance your financial resilience and help you achieve your financial aspirations.

Conclusion: Taking Control of Your Financial Future

Adopting the 50/30/20 rule is a meaningful step toward financial security. This simple yet effective method can guide you in managing your income wisely. It’s not just about percentages but a way to prioritize your spending and savings goals.

By aligning your financial habits with the 50/30/20 rule, you start a journey toward informed money management. This can lead to reduced stress and enhanced financial confidence. With consistent effort and adaptation, you’re empowered to shape a future that reflects your financial aspirations. Take charge today and set the foundation for a prosperous tomorrow.